The average cost of sending a $200 remittance is 6.5%. With stablecoins, total cost drops below 1% and funds arrive in seconds. Fintechs and smaller banks can now launch competitive remittance services, and institutions already offering remittances can serve corridors and customer segments that previously weren’t economical. This article explains how stablecoin remittances work, how to evaluate if they fit your business, and how to launch a pilot. If you’re ready to get started, get in touch.

For millions of people, remittances are a lifeline: regular payments sent home to support families, fund education, or cover essential expenses. According to World Bank estimates, the global remittance market moves over $900 billion annually, with 200 million people sending money home each year[1].

Stablecoins have opened remittances to fintechs and smaller banks, without requiring correspondent banks. Moreover, in many corridors, dollar demand outstrips local supply, giving them a structural FX advantage over incumbents through liquidity premiums.

Companies like DolarApp, Félix Pago, and Chipper Cash are already using stablecoins to power remittances across Latin America and Africa. They are offering consumers lower fees, better exchange rates, and money that arrives in seconds, capturing market share from legacy players.

Why traditional rails are prohibitively expensive

For fintechs and smaller banks looking to offer remittances, traditional correspondent banking creates barriers and adds cost at every step:

- Correspondent relationships are difficult to obtain. To send a remittance to Mexico, an institution needs a banking relationship with a correspondent that has access to Mexico’s local payment rails. Large banks are de-risking, refusing to onboard smaller institutions to avoid compliance overhead. Those without correspondent access must use intermediaries who might charge 10x more.

- Unit economics are broken. According to World Bank data, the global average cost of sending a $200 remittance is 6.5%[2]. Domestic fast payment systems typically cost less than 1%. That gap is the correspondent banking tax: each intermediary adds processing overhead, compliance costs, and margin.

- FX rates are dictated by correspondents. Smaller institutions have no leverage to negotiate competitive foreign exchange rates. This hidden cost gets passed to customers or absorbed as margin compression, and there is no practical way to shop for better rates without building additional banking relationships.

- Liquidity sits frozen in nostro accounts. Correspondent banking takes days to settle, but customers want their money fast. The only solution is pre-funding local currency accounts in every destination. McKinsey estimates this trapped capital represents 34% of international payment costs[3].

For institutions already offering remittances, expansion is expensive. Each new corridor means new correspondent relationships, more pre-funded accounts, and additional compliance overhead. Many corridors simply are not worth the investment.

How stablecoins enable remittances

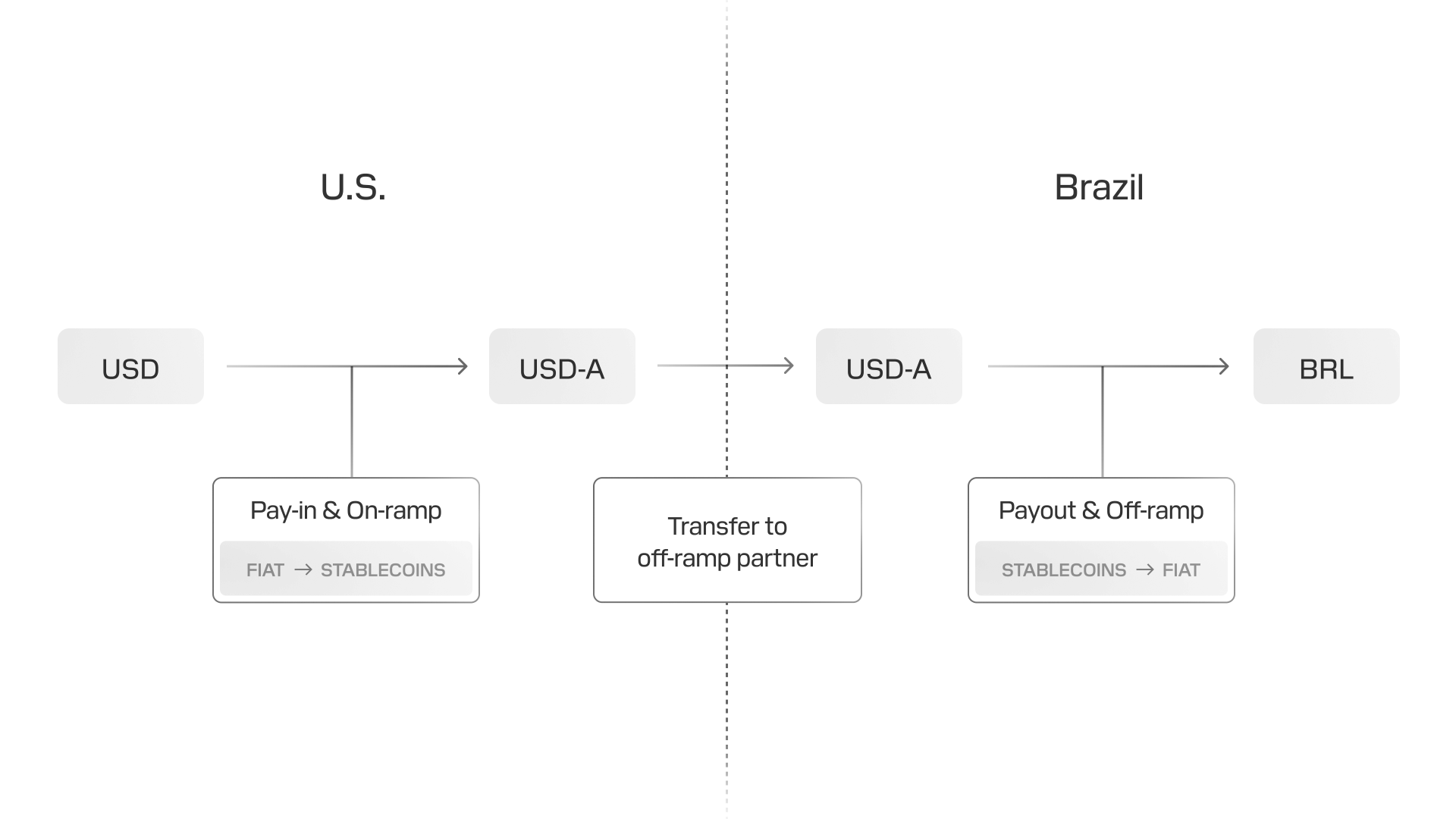

Stablecoins change how cross-border payments work. Instead of relying on correspondent banks, the flow is simpler: local currency is converted to stablecoins, transferred on a blockchain, then converted back to local currency at the destination. This approach is often called the “stablecoin sandwich”.

Access without banking partnerships

Institutions do not need permission from large banks to access their payment networks. They need an orchestration partner that provides on-ramps to convert local currency to stablecoins and off-ramps to convert stablecoins back to local currency at the destination. These are competitive service providers, not gatekeepers.

Costs that enable competitive pricing

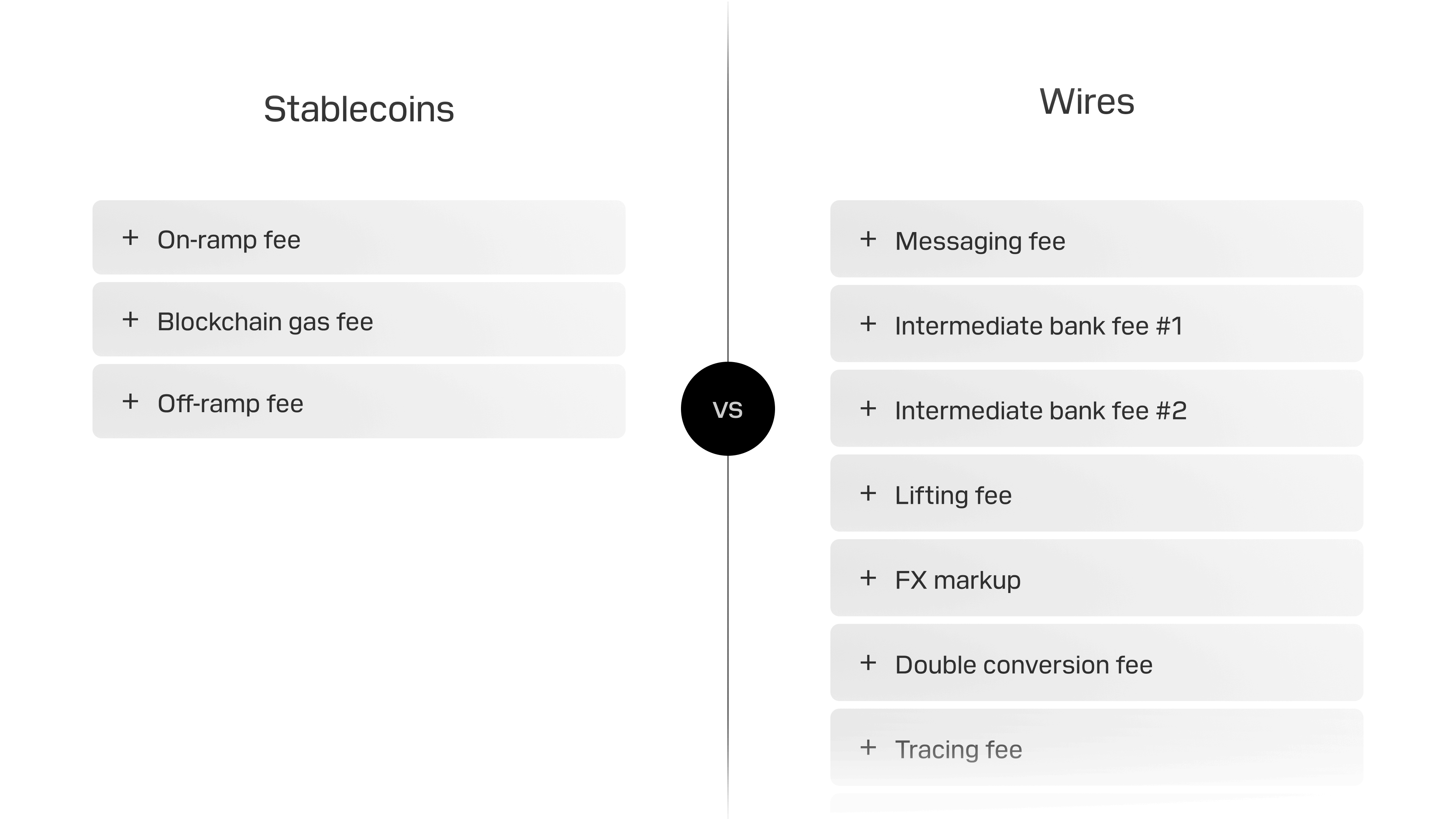

Stablecoin remittances have three fee components: on-ramp conversion (0.1-0.5%), blockchain fees (under $0.01), and off-ramp conversion (0.1-0.5%). A total cost under 1% means remittance providers can undercut legacy pricing while still maintaining a healthy margin.

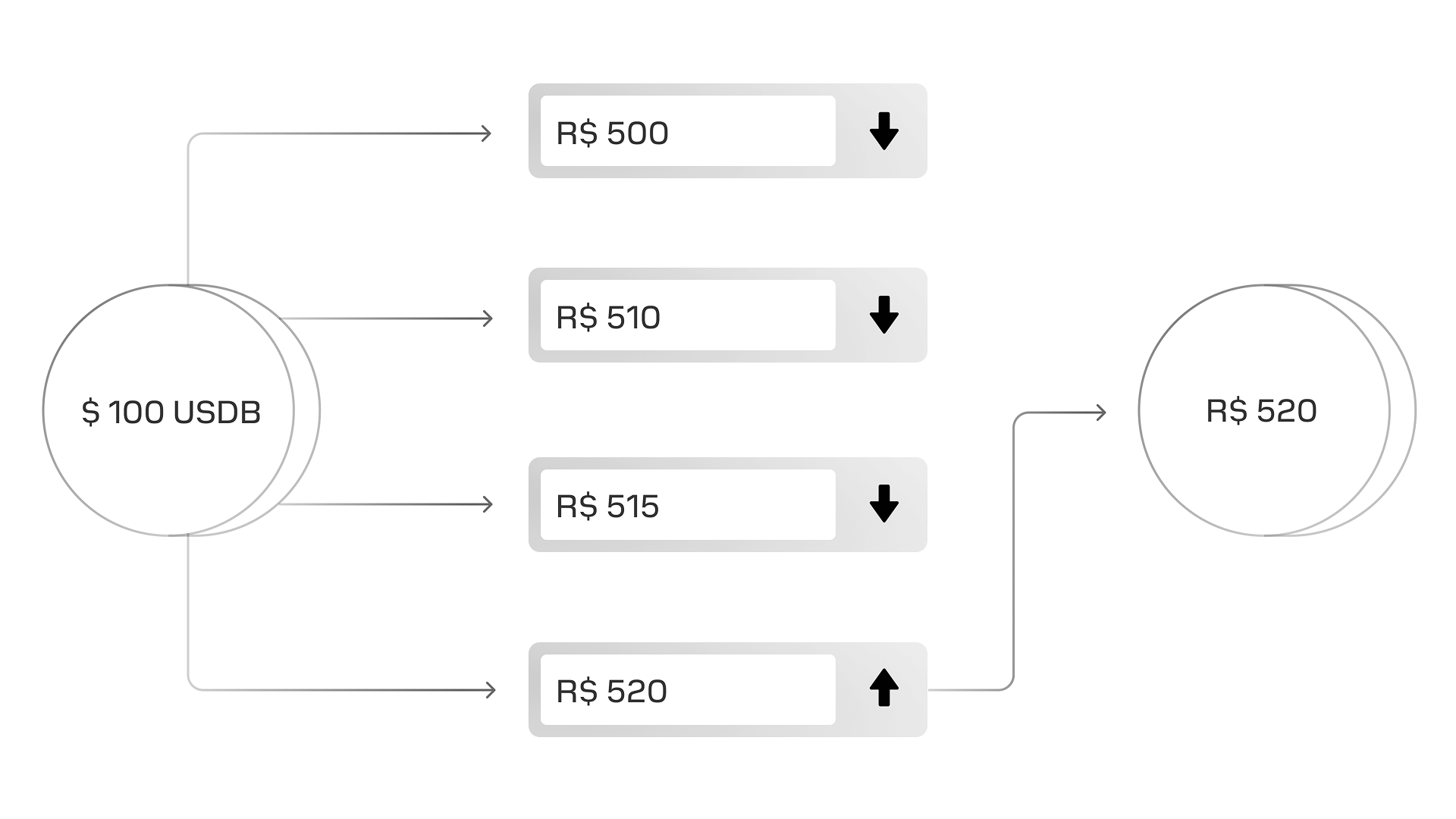

Cheaper FX through the USD demand premium

In many markets, demand for US dollars outstrips local supply, creating a 20–200 bps FX premium for USD stablecoins above market rates, depending on the corridor. Instead of being locked into one correspondent bank, remitters can work with multiple off-ramp providers who compete on rates, passing that margin directly to customers.

Access to long tail markets

Correspondent banking only works for high-volume corridors. Stablecoins open up smaller markets because the infrastructure cost is the same whether you are sending to Mexico or Mongolia. If an off-ramp exists, the corridor is open.

Settlement in seconds, without pre-funding

Stablecoins settle near-instantly, eliminating the need for pre-funded accounts in every destination country. No trapped capital, no multi-day uncertainty. Customers see their transfer complete in real time.

Evaluating stablecoins for remittances

Stablecoin adoption starts with a clear business case. Before evaluating orchestration partners or integration paths, use this framework to assess whether stablecoins make sense for your remittance offering:

- Are your customers already using remittances? If you are seeing outflows to Wise, Remitly, Western Union, or similar services, your customers are sending money abroad, just not through you.

- Are you blocked from offering remittances today? Correspondent banking relationships, SWIFT infrastructure costs, or compliance overhead can make it impossible to build a remittance product that competes on price and speed.

- Already offering remittances, but cannot compete on experience? Traditional rails mean customers send money and wait days without knowing if or when it will arrive. This generates support tickets, complaints, and manual follow-ups that drain operational resources.

- Would faster, cheaper remittances strengthen customer retention? Remittances are a frequent, high-value touchpoint. Offering instant settlement at lower fees can deepen relationships, increase wallet share, and differentiate you from competitors.

If the answer to these questions is yes, you should be evaluating stablecoins. The infrastructure is ready, regulation is clearer, and the economics are compelling.

Getting started with stablecoins

You can start with a single corridor, validate unit economics, track adoption, and scale once the business case is proven. Here’s how to approach it:

Step 1: Pick your corridor

Start with one remittance corridor that matters to your customers. Look at your payment outflows to identify where customers are using third-party remittance services. Survey a sample of these customers to understand which corridors they’re using most. Focus on corridors with high volume or poor customer experience (long settlement times, high fees, frequent complaints).

Step 2: Choose your integration approach

Decide whether to partner with an orchestration provider or build your own infrastructure. Partners handle on-ramps, off-ramps, liquidity sourcing, compliance, and custody, letting you integrate via API in weeks. Building in-house gives you more control, but the biggest hurdle is often licensing: obtaining money transmitter licenses, virtual asset service provider registrations, or equivalent authorizations in every jurisdiction you operate in.

Step 3: Start with wholesale on-ramp and off-ramp

You do not need to process each remittance individually from day one. Batching transactions (converting to and from stablecoins in bulk) offers better rates, but slower settlement. It is a practical way to validate a corridor and build operational confidence. Just be ready to move to per-transaction processing shortly, as competition and customer expectations will require instant settlement.

Step 4: Pilot alongside existing rails

If you already have SWIFT connectivity or correspondent banking relationships, keep them. Run stablecoins in parallel. Offer a subset of customers the option to receive funds via stablecoins instead of traditional rails. Let them experience faster settlement and lower fees. Run the pilot for 60-90 days to validate cost savings, identify operational gaps, and gather customer feedback before committing to scale.

Step 5: Ensure compliance

Work with your orchestration partner or legal team to ensure compliance with the Travel Rule and local regulations. The Travel Rule requires transmitting customer information with transactions above certain thresholds. Your partner should handle this as part of their service, or you’ll need to implement it yourself. Also verify that your chosen corridors and on/off-ramp providers meet local licensing requirements.

Risks and limitations

Stablecoins solve fundamental problems with traditional remittance rails, but they introduce their own constraints. Here is what to consider:

- Regulatory coverage is uneven. Some corridors have clear stablecoin regulations. Others are in regulatory gray zones or explicitly prohibit stablecoin use for payments. Before piloting a corridor, verify that both the sending and receiving jurisdictions permit stablecoin-based money transmission.

- Off-ramp availability varies by geography. An orchestration partner may not have local off-ramp coverage in every required country. Tier-1 corridors like the U.S. to Mexico or the U.S. to the Philippines have mature liquidity. Less common corridors may have limited off-ramp options, higher conversion costs, or longer settlement times that erode the stablecoin advantage.

- New infrastructure means new failure modes. Stablecoin rails introduce dependencies that do not exist in traditional payments: blockchain uptime, smart contract risk, wallet custody, and API reliability from on/off-ramp partners. Each is a potential point of failure requiring monitoring, fallback procedures, and updated support processes.

- Economics break down at low volumes. On-ramp and off-ramp providers typically charge percentage-based fees. At scale, these fees are competitive with traditional rails. At low corridor volumes, they can be prohibitive. If an institution processes a few transactions per month in a corridor, the unit economics may not justify the integration effort.

- Regulators may require additional reporting. Many regulators are still building familiarity with stablecoin infrastructure. Even in jurisdictions where stablecoins are legal, institutions may face extra reporting requirements, audits, or documentation requests that would not apply to traditional remittance rails. Institutions should budget time for compliance conversations and expect iteration as regulatory expectations evolve.

Work with Tempo

Tempo’s enterprise team helps banks and fintechs evaluate and implement stablecoins as part of a modern remittance strategy, from initial analysis through pilot and scale.

- Analyze your payment outflows to identify high-impact corridors

- Model the business case with your transaction data

- Review integration requirements for your tech stack

- Design a pilot program tailored to your operational needs

- Connect you with institutions that have launched stablecoin remittances

If you’d like to explore stablecoin remittances with our financial services consulting and product teams, contact our Enterprise Team.

[1] Source: 2025 Digital Remittances Adoption Report

[2] Source: World Bank Remittance Prices Worldwide

[3] Source: Global Payments 2016: Strong Fundamentals Despite Uncertain Times

FAQs

Do institutions have to hold and manage stablecoins?

No. Stablecoin orchestration providers like Bridge and BVNK abstract the complexity of managing stablecoins, wallets, and licensing. Institutions connect to the provider’s API to instruct a remittance, send funds from a bank account in fiat currency, and they handle on-ramp, off-ramp, custody, and liquidity management.

Will recipients understand stablecoins?

They do not have to. Modern stablecoin infrastructure can be invisible to end users. Recipients get a notification that payment arrived and see a balance in their local currency or USD in a mobile app. The underlying blockchain technology is abstracted away.

What currency does the recipient receive?

The recipient receives local currency directly in their bank account or mobile wallet. The orchestration partner handles the stablecoin conversion automatically behind the scenes. From the recipient’s perspective, it works exactly like a traditional remittance: they get a notification and see local currency available for withdrawal or use.

How does the Travel Rule work for stablecoin remittances?

The Travel Rule requires transmitting customer information with transactions above certain thresholds (typically $1,000 in the U.S.). The orchestration partner should handle Travel Rule compliance as part of their service. If building in-house, institutions need to implement Travel Rule protocols directly and ensure compliance in each jurisdiction.

Is this regulated?

Yes. Stablecoin remittances are subject to money transmission regulations in most jurisdictions. Any institution offering remittance services must comply with KYC/AML requirements, Travel Rule obligations, and obtain appropriate licenses. Regulatory clarity has improved significantly, particularly in the U.S., following recent legislation.