Stablecoins settle instantly, 24/7, across borders. For companies that run global payouts, that means faster delivery, lower fees, and fewer steps to pay recipients. This guide explains the benefits for businesses evaluating stablecoins to simplify their payout operations. Contact us if you’re evaluating stablecoins for global payouts.

For any business operating globally, whether a marketplace paying thousands of merchants or a software company with a distributed team, payouts are operationally complex. Stablecoins simplify this by enabling dollar-based payouts to over 140 countries, arriving in seconds. Recipients receive funds in a stablecoin-compatible wallet, giving them control, speed, and stability.

The costs of traditional cross-border payouts

Consider an example: when you send $1,000 to a contractor in Brazil using traditional rails, the costs add up quickly. Your payment processor may charge a $10–40 fee per payment, while intermediary banks take anywhere from 0.1% to 4.0% on the FX spread. By the time the payment clears five days later, the recipient has lost $80 to fees. If local currency moved adversely in that window, they would lose again.

The friction falls into predictable categories:

- High transaction costs: A single cross-border payment can pass through three or four intermediary banks, each taking a cut. When multiplied by thousands of payouts, these fees erode margins for the company and reduce the take-home pay for the recipient.

- Slow, unpredictable settlement: Payouts can take 3-5 business days to arrive, complicated by time zones, bank holidays, and compliance checks. This uncertainty makes cash flow management difficult for recipients who rely on timely payments.

- Payout failures and reconciliation overheads: A simple data entry error can cause a payment to fail, leading to a lengthy and manual reconciliation process. For finance teams, tracking and resolving thousands of individual payments creates a significant operational burden.

- Currency volatility risk: Recipients in emerging markets are often exposed to the volatility of their local currency. A payment that was worth $1,000 when sent might be worth significantly less by the time it arrives and can be converted, unfairly penalizing the earner.

How stablecoins improve global payouts

Stablecoins bypass the correspondent banking system entirely, enabling direct payouts to any worker or contractor with a compatible wallet. Stablecoin payments settle in seconds, 24/7, without being constrained by banking hours, public holidays, or time zones.

When you send $1,000 to a contractor in Brazil using stablecoin rails, the process is far more straightforward: your stablecoin partner may charge a flat fee of 0.1–0.4% for the onramp and transfer, delivering a ~60–80% cost reduction[1] compared to traditional rails.

Recipients receive dollar-denominated stablecoins and can convert to local currency when and how they choose, typically paying a transparent offramp fee in the 0.1–2.0% range. The benefits are concrete:

Instant settlement

Stablecoins are powered by blockchains that operate 24/7/365, and stablecoin payouts settle in seconds, not days. This means workers and merchants get paid on time, every time, improving satisfaction and retention.

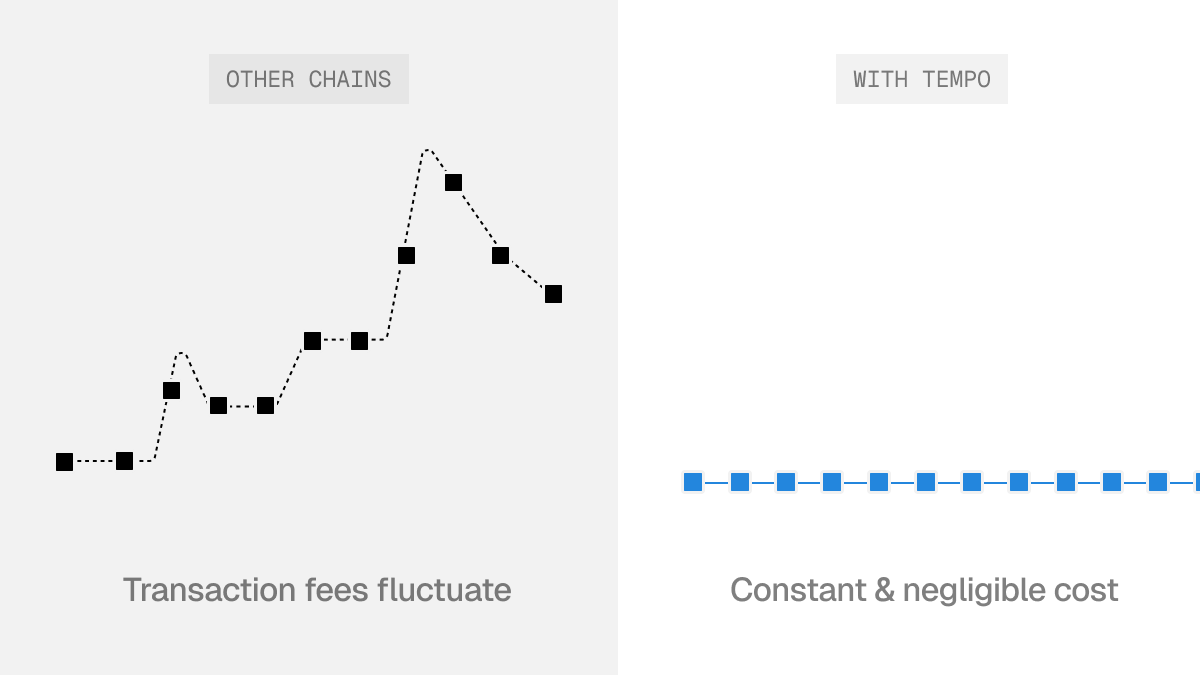

Lower costs

By eliminating intermediaries, stablecoins can reduce the cost of a cross-border payment by at least ~60-80%. This allows platforms to save on operational costs or pass the savings on to their users.

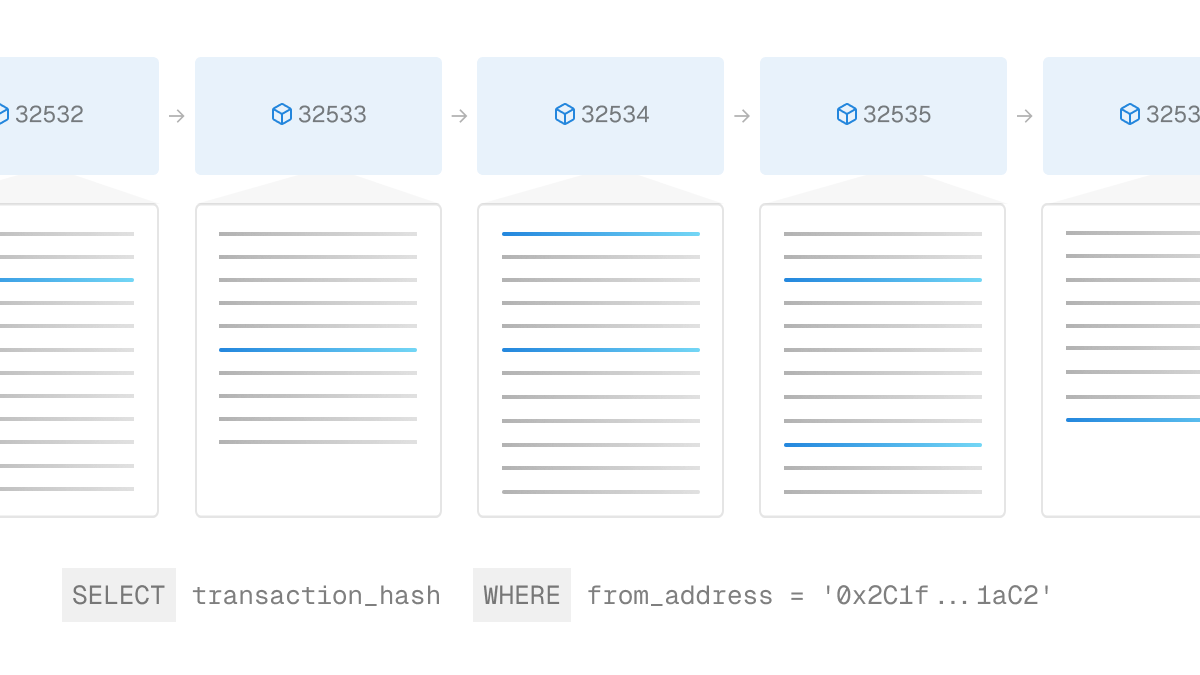

Traceability

Every stablecoin transaction is recorded on the blockchain, creating an immutable audit trail that can be tracked in real-time by both payers and payees. This reduces disputes and simplifies reconciliation.

Dollar-based stability

Payouts sent in US dollar-denominated stablecoins protect recipients from local currency devaluation. They receive a stable store of value and can convert to their local currency on their own terms.

Broader access

Stablecoins can be sent to any compatible digital wallet, anywhere in the world. This opens access to global economic opportunities for individuals in countries underserved by traditional banking.

Evaluating stablecoins for global payouts

Stablecoin adoption starts with a clear business use case. Before evaluating vendors or integration paths, here is a helpful framework for evaluating stablecoins for global payouts:

- Do you pay people internationally? If you are paying contractors, merchants, or employees across borders, you are already managing multiple currencies, banks, and regulatory regimes.

- Do those payments create friction today? Delays, failed transfers, opaque fees, FX leakage, and reconciliation errors are signals that your current payout rails are not keeping up.

- Are you forced to pre-fund payouts? Long settlement times often require holding excess balances across banks and currencies, tying up working capital.

- Would reducing that friction materially impact your business? Faster payouts, lower costs, and happier recipients can improve retention, reduce operational overhead, and unlock new geographies.

- Can instant payouts become a new revenue stream? Many platforms offer real-time payouts as a premium feature, turning speed and reliability into a paid upgrade rather than a cost center.

If the answer to these questions is yes, you should be evaluating the stablecoin partner ecosystem. The infrastructure is ready, regulation is clearer, and the economics are hard to ignore.

Getting started with stablecoins

Payouts are one of the cleanest entry points for stablecoins: easy to pilot and deliver immediate, measurable impact. Teams can start with a single corridor, validate speed and cost improvements quickly, and scale once the business case is proven. Here’s how to get started:

Step 1: Clarify the business case

Pick your highest-friction payout corridor, such as the U.S. to the Philippines, Nigeria, or Brazil. Identify a segment of contractors that are frustrated with delays and fees in the current system. Offer them instant payouts with 60–80% lower fees. You can start manually or move directly into a pilot to test the impact at scale.

Step 2: Identify an integration approach

Decide whether to partner with a third party or build infrastructure yourself. Partners can simplify implementation by handling blockchain selection, liquidity sourcing, custody, and other operational complexities. Companies that build in-house must assemble their own stack: wallets, custody, liquidity, bank relationships, and potentially MTL or similar local licenses.

Step 3: Pilot stablecoins for payouts

Run a pilot. Integrations can take as little as two weeks, with providers like BVNK, ZeroHash, or Bridge handling the underlying infrastructure. Add a small number of API calls to your existing payout flow and run stablecoin payouts alongside your existing system for 60 days to build confidence before scaling. Pilots quickly reveal benefits as well as operational complexities like customer support needs, integration gaps, or errors.

Step 4: Operationalize

Turn the pilot into a standard payout flow. Lock in processes across finance, ops, support, and compliance, including SLAs, reconciliation, treasury management, and exception handling. Train support teams on how stablecoin payouts work. Then expand to new corridors and segments, increase volumes, and automate what was manual during the pilot.

Work with Tempo

Tempo’s enterprise team helps companies evaluate and implement stablecoins as part of a modern global payouts strategy, from initial analysis through pilot and scale.

- Analyze your operations to identify high-value use cases

- Model the business case with your transaction data

- Review integration requirements for your tech stack

- Design a pilot program tailored to your operational needs

- Connect you with companies that have implemented stablecoin payouts

If you’d like to explore stablecoin payouts with our financial services consulting and product teams, get in touch with our Enterprise Team.

Frequently Asked Questions

Do I have to hold and manage stablecoins?

No. Many infrastructure providers, such as BVNK, Bridge, and ZeroHash, abstract the complexity of managing stablecoins, wallets, or licensing. You connect to their API to instruct a stablecoin payout, send funds from your bank account in fiat currency, and they handle on- and off-ramp, custody, and liquidity management.

Will recipients understand stablecoins?

They don’t have to. Historically, stablecoin payouts were used primarily by crypto-native developers and contractors. That is changing as new fintech apps hide the complexity. Modern stablecoin infrastructure, like embedded wallets, can be invisible. The recipient gets a notification that payment arrived and sees a balance in US dollars on a mobile app.

What happens if a recipient wants local currency?

Recipients can convert stablecoins to local currency through supported off-ramps as soon as funds arrive. This is often a one-click experience inside a fintech app or exchange, with transparent fees that are typically far lower than traditional bank FX spreads. Stablecoin orchestration platforms can also automate this process end-to-end.

Is this only useful for emerging markets?

No. While the benefits are most visible in emerging markets with high fees or volatile currencies, stablecoin payouts are increasingly used in developed markets as well, especially for instant payouts, weekend payments, or premium payout features.

Is this regulated?

Yes, increasingly so. Since the passage of the GENIUS Act in the United States, the compliance landscape for stablecoins has become clearer. Any money transmitter, financial institution, or nonbank money mover is subject to travel rule requirements. In practice, regulatory requirements like KYC/KYB and screening of senders over $1,000 are lower risk in payout use cases because the payer is the corporation itself.

[1]* Cost reduction calculation: Traditional cross-border wire fees on a $1,000 payout typically range from $10–40 (1.0–4.0%) excluding FX spreads. Stablecoin onramp fees range from 0.1–0.4%. Comparing the high end of stablecoin costs (0.4%) against the low end of wire costs ($10/1.0%) yields a 60% reduction. The upper range reflects comparisons against higher wire fees and FX spreads.*