Sponsor banks already power fintechs with bank accounts, virtual accounts, and payments. The same fintechs now need stablecoin wallets, transfers, and cards. Sponsor banks that build for this can defend their customer base and grow revenue per relationship. Get in touch if you are a sponsor bank evaluating stablecoin services for your fintech customers.

The last decade of fintech ran on sponsor banks. Banks like Cross River, Coastal, and Lead and others gave fintechs access to the regulatory and operational rails that they couldn’t access on their own: bank accounts, payments, and cards, packaged behind modern APIs. Fintechs owned the customer relationship while their bank partners provided the charter, the balance sheet and access to payment rails. Banks that successfully adopted this partnership model have realized above-market return on equity over the past decade.

Fintech companies are now coming onchain. Their customers now also want stablecoin accounts, instant cross-border payments, and onchain savings products. Stablecoin supply has crossed $300 billion1. McKinsey & Company tracked more than $390 billion2 in real payment volume over the past year. Visa hosts more than 160 stablecoin card programs globally and settles $7 billion in annualized stablecoin card payment volume, which is up nearly 200% year-over-year3.

Supporting stablecoin-backed business models is now a golden opportunity for sponsor banks. The passage of the GENIUS act in the US and MiCA in Europe have cleared the regulatory path. Regulators across the globe have given banks the greenlight to build on stablecoin infrastructure. Sponsor banks already have the relationship, the compliance program, and the integration in place for fintech programs. Extending into stablecoins deepens existing relationships and opens new revenue streams.

What fintechs are asking for

Remittance companies already use stablecoins to save on fees or serve long-tail corridors. PSPs sell global payouts with stablecoins to marketplaces. Neobanks let users hold savings in dollars with stablecoins, especially in markets with high inflation.

The growing number of use-cases presents an opportunity for sponsor banks to handle the whole stack:

-

Custodial stablecoin accounts for fintechs and their end-users. The bank retains control over onchain accounts with stablecoin balances landing on its books, the same way DDA and FBO programs work for fiat.

-

Onramp and offramp between fiat and stablecoins. Funds flow via ACH or card the same way they do for DDA accounts, but get credited to custodial wallets in stablecoins. The conversion step is a new piece.

-

Stablecoin payment origination for domestic or cross-border payments. Payments are sent and received on behalf of fintech customers, including flows routed through the so-called stablecoin sandwich. Same role banks already play in ACH and wire payments.

-

Stablecoin card programs. Authorization runs in real time against the cardholder’s onchain balance in the custodial account, not a fiat DDA. BIN sponsorship and program management carry over directly from fiat debit and prepaid cards.

-

Savings products. Customers earn interest on their stablecoin balance, with returns sourced from tokenized money market funds or DeFi protocols. Same product as a fiat high-yield savings account, except the yield passes through directly from the fund or protocol rather than the bank’s NIM on deposits.

A fintech that wants this stack has two options. Find new vendors and build a parallel onchain program on top of their sponsor bank’s fiat offering. Or ask their sponsor bank to expand the relationship to cover both.

The second option is the cleanest for the fintech and the most defensible for the bank. A single compliance program, a single contract, a single API integration, fiat and stablecoins on the same statement.

Why banks choose to build on Tempo

Tempo is built for payments, with high throughput, predictable low fees, and fees payable in stablecoins instead of a native gas token. However, several features were designed specifically for financial institutions, and they map directly to how sponsor banks already work.

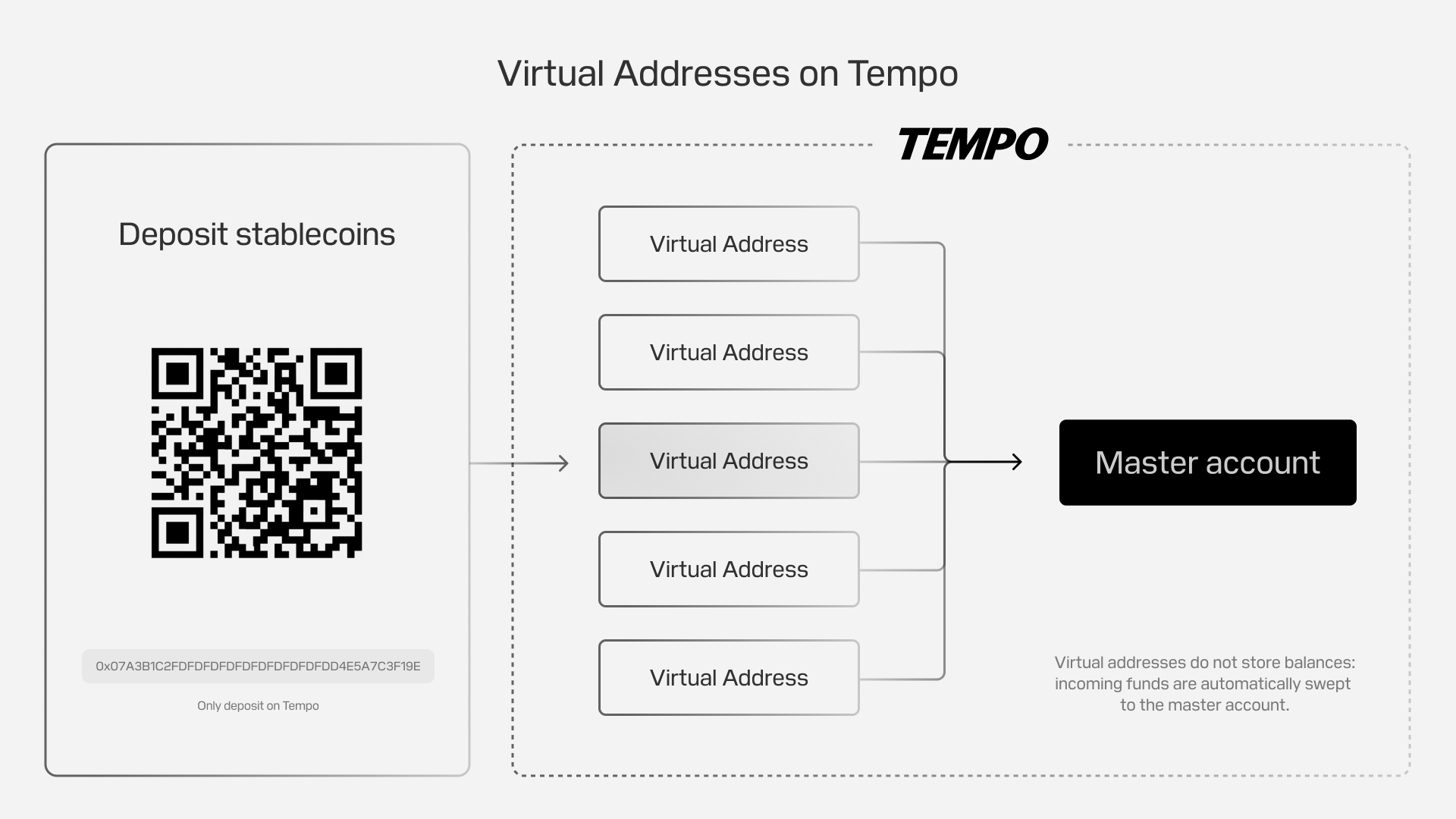

- Virtual addresses are the onchain analog of virtual account numbers. A sponsor bank registers a master wallet for each fintech, creating an equivalent of an FBO account, and then derives a unique receive address for every fintech end-user. Inbound transfers route to the master wallet automatically, with no sweep step. Reconciliation works the same way it does for virtual accounts.

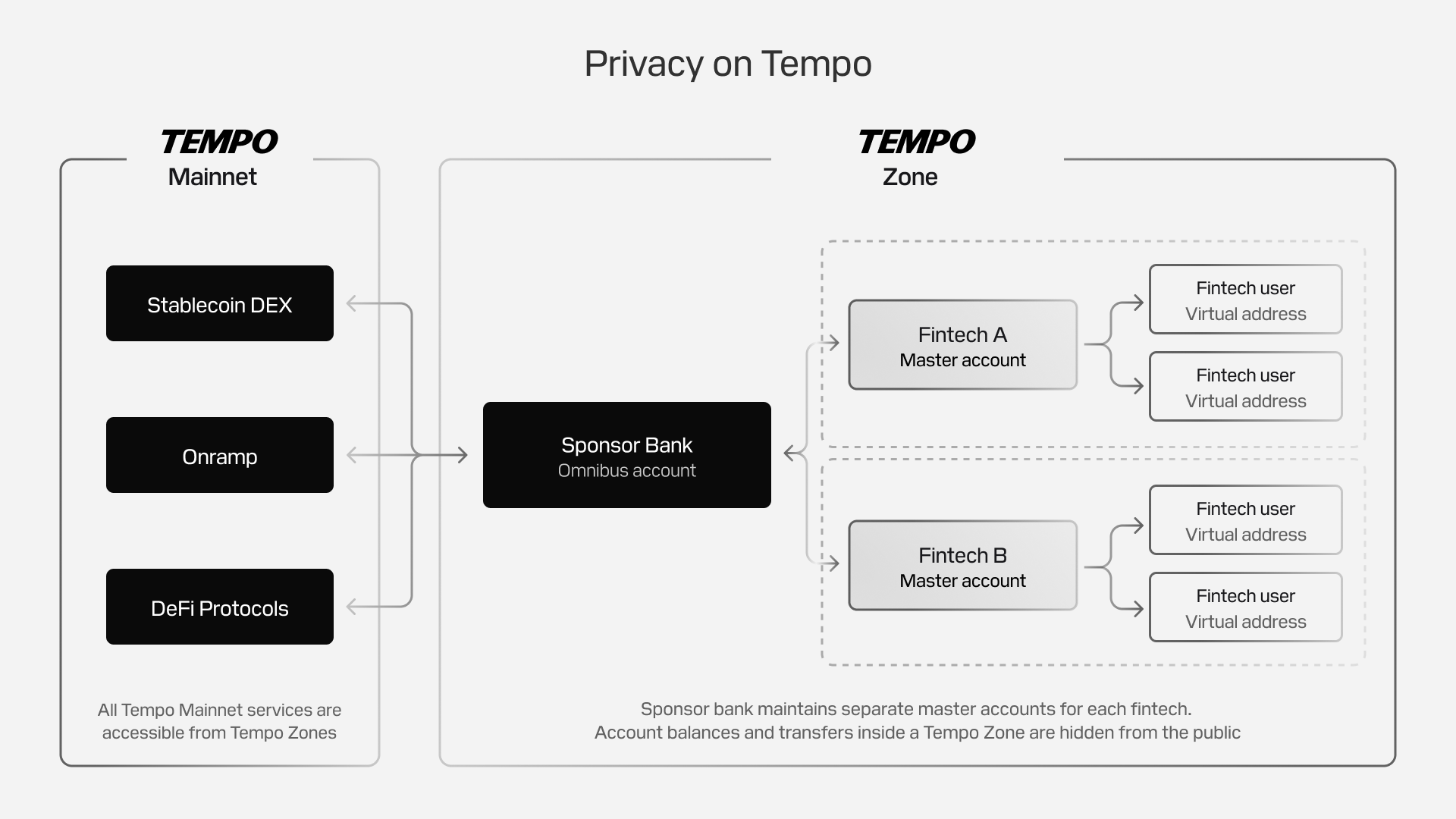

- Tempo Zones give regulated institutions privacy at the protocol level. Account balances and transactions stay confidential while remaining auditable for the bank and its regulators. A sponsor bank can run its own zone or use a partner-operated one.

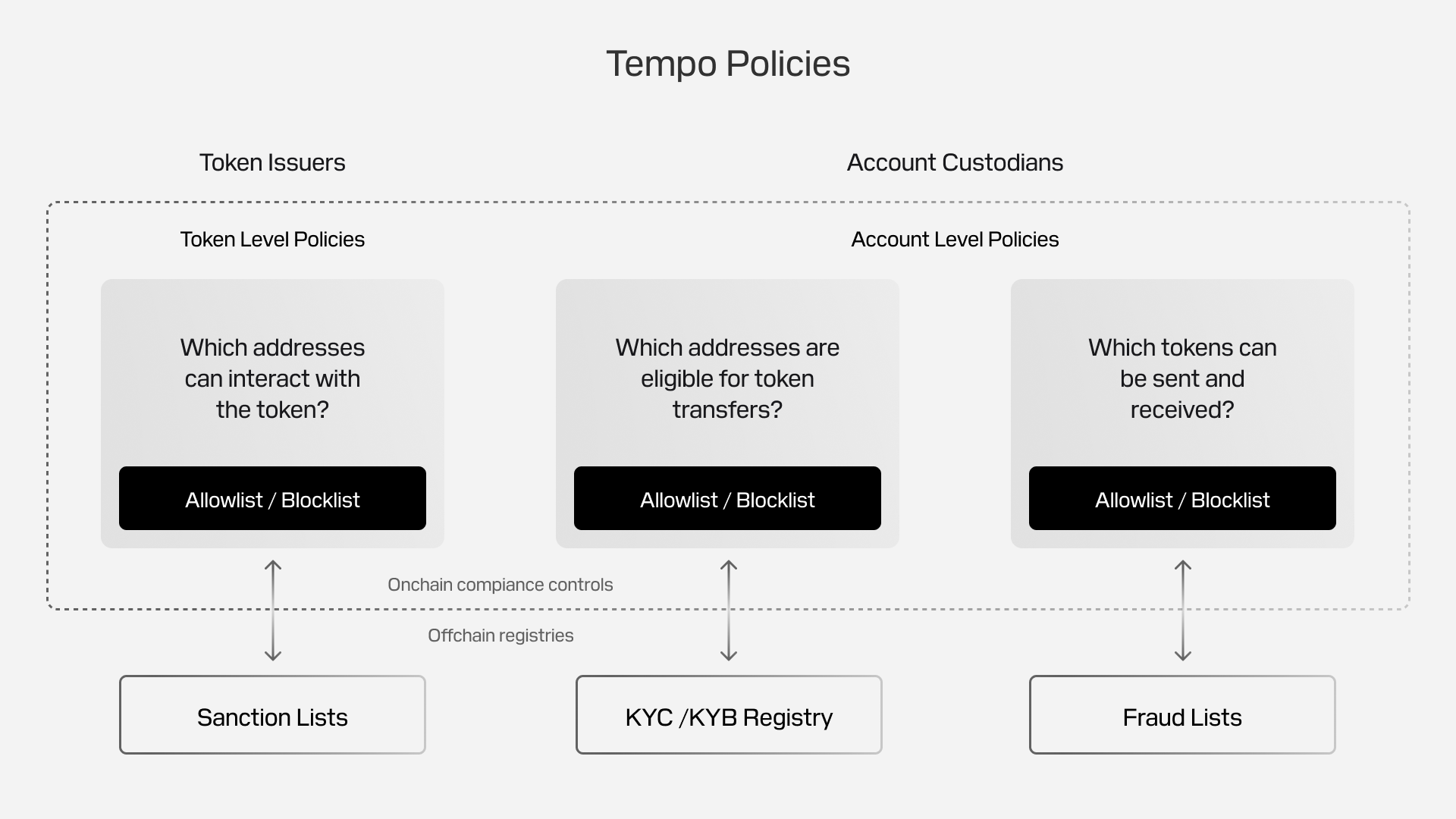

- Compliance controls are native to the protocol. Token-level allowlists and blocklists let issuers gate stablecoins to KYC’d users. Account-level policies, rolling out soon, let custodial wallet operators (sponsor banks among them) restrict which addresses a wallet can transact with and which tokens it can hold.

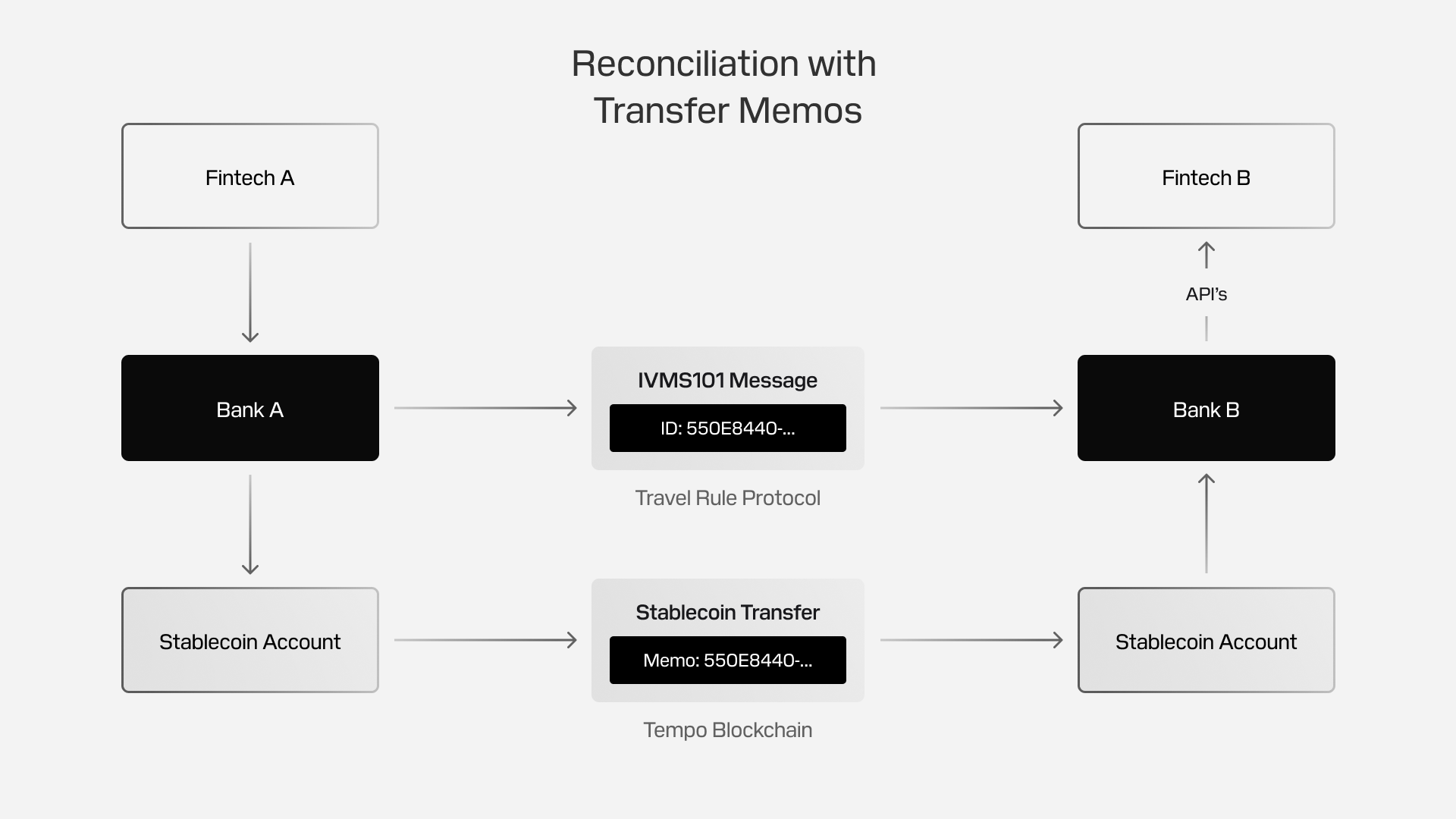

- Transfer memos are additional information attached to any native token transfer on Tempo. Transfer memos can be used for reconciliation across onchain and offchain rails, for example, to reconcile stablecoin transfers with IVMS101 and SWIFT messages.

More than 60 partners have already integrated Tempo features across custody, wallets, onramps and offramps, compliance, cards, and savings. Sponsor banks can compose a stack from the ecosystem rather than build one to accelerate development.

How to build it

Sponsor banks don’t need to ship the full stack on day one. Pick a fintech client or segment with clear stablecoin demand and build for them first. The rest of the book follows.

-

Start with a minimum viable offering. Onramp and offramp paired with custody is enough to launch. The ability to hold, send, and receive stablecoins covers many use cases, from global trade to cross-border payouts. Cards and savings can come later.

-

Partner for wallets. Wallet infrastructure is fundamentally a security problem with multi-chain complexity. Key storage, transaction signing, and account recovery are easy to get wrong, and getting them right requires a crypto-engineering team most banks don’t have. Privy, Turnkey, and Crossmint run embedded and custodial wallet platforms covering authentication, key management, signing, recovery, and multi-chain support.

-

Line up issuers for onramp. The sponsor bank is already the fiat leg of the onramp through ACH and wires. The missing piece is a direct mint and redemption relationship with stablecoin issuers. Consider holding pre-minted inventory for real-time user onramps. Orchestration platforms like Bridge and BVNK enter the picture later, when fintechs need to serve markets outside the US or in non-USD currencies.

-

Extend the compliance program. Your fiat AML and sanctions tooling carries over. What’s new onchain is screening for sanctioned addresses, monitoring counterparty wallets, and applying the Travel Rule to stablecoin transfers. Vendors like Chainalysis, TRM, and Sardine plug into the case management your team already runs.

-

Scope the rollout. Launch with a small number of fintech partners who already serve the use cases that fit. Run them on real volume for 60 to 90 days. Use what you learn to harden the product before opening it to the rest of your book.

Once the core products are live, collect feedback from fintech partners and their end-users on what’s actually being used, where flows break, and what they ask for next. Use that feedback to prioritize the next layer of products. Some emerging product and revenue opportunities include:

-

Add stablecoin cards. Stablecoin cards are the fastest-growing stablecoin product. They let consumers and businesses spend stablecoins anywhere a card is accepted. Consider settlement with the card networks in stablecoins as well.

-

Source the savings yield. Onchain yield comes from tokenized money market funds or DeFi lending protocols like Aave and Morpho. Most sponsor banks won’t offer these products themselves, so set up partnership early. This is usually the next ask after launch.

-

Enable merchant payouts. PSPs and marketplaces can pay merchants in seconds, not days. Merchants get working capital sooner, and the platform can offer instant payouts as a premium feature. Build capabilities to enable mass stablecoin payouts.

-

Add non-USD, FX, and custom stablecoins. USD stablecoins are the starting point. The next layer is non-USD stablecoins and onchain FX between them. Tailor the offering for local markets and use cases.

Several areas need answers before launch. Who custodies the stablecoins and on whose books they sit. How reconciliation handles a payment that can arrive onchain or via wire. How suspicious activity reporting works for onchain flows. Which stablecoins the program supports, and on which networks. Discovering the answer after launch is expensive.

Work with Tempo

Tempo supports sponsor bank stablecoin programs through advisory, native protocol features, and a partner ecosystem. That includes designing the use case, bringing the right partners, and developing missing blockchain features when needed.

-

Stablecoin Advisory. Tempo’s advisory team helps sponsor banks scope the offering, select partners, design the compliance program, and run the first pilot. Learn about Tempo’s Stablecoin Advisory.

-

Native protocol features. Tempo builds capabilities critical to real-world use cases, like privacy and compliance, directly into the protocol. That removes the need for application-layer workarounds. Read the docs and try demos.

-

Partner ecosystem. Whether finding wallet partners, lining up issuers, sourcing savings yield, or extending the compliance program, Tempo’s partner ecosystem covers it. Tempo continues to bring in new partners as use cases emerge. Explore the ecosystem.

If you’re a sponsor bank evaluating stablecoin services for your fintech customers, see what companies are building on Tempo and get in touch with our Enterprise Team.

Footnotes

Frequently asked questions

What fintechs are asking for?

Remittance companies already use stablecoins to save on fees or serve long-tail corridors. PSPs sell global payouts with stablecoins to marketplaces. Neobanks let users hold savings in dollars with stablecoins, especially in markets with high inflation.

Why banks choose to build on Tempo?

Tempo is built for payments, with high throughput, predictable low fees, and fees payable in stablecoins instead of a native gas token. However, several features were designed specifically for financial institutions, and they map directly to how sponsor banks already work.

How to build it?

Sponsor banks don't need to ship the full stack on day one. Pick a fintech client or segment with clear stablecoin demand and build for them first. The rest of the book follows.

What does the article say about Work with Tempo?

Tempo supports sponsor bank stablecoin programs through advisory, native protocol features, and a partner ecosystem. That includes designing the use case, bringing the right partners, and developing missing blockchain features when needed.